Jewellery valuations — Adelaide

Know what it takes

to replace it.

A valuation is a formal, documented record of what your jewellery would cost to replace today — the document your insurer relies on if a piece is ever lost, stolen or damaged. Ours are carried out independently, which is exactly how a valuation should be done.

Why independence matters

A valuation should have no agenda.

A valuation is only worth what its independence is worth. If the person valuing your jewellery also wants to buy it from you, or sell you something in its place, the number carries an interest — theirs. That is why our valuations are carried out at arm’s length by NCJV-registered independent valuer with no stake in the piece: not in buying it, not in selling it, not in what the number turns out to be.

The value of your jewellery should be a finding, not a pitch.

When you need one

The moments that call for a valuation.

A new or significant piece

An engagement ring, an heirloom passed to you, a piece you have had made — anything you would want properly covered from day one.

An out-of-date valuation

Gold and stone prices move, so a valuation ages. Updating it every two to three years keeps your cover honest — a piece valued years ago can cost far more to replace today.

Before and after restoration

For antique pieces we often recommend a valuation before work begins and an updated one after, so your insurance reflects the piece as it is now.

Estates and settlements

Wills, estates and legal settlements need a documented, defensible value from someone with no interest in the outcome. Independence matters most here.

What you receive

A document your insurer can act on.

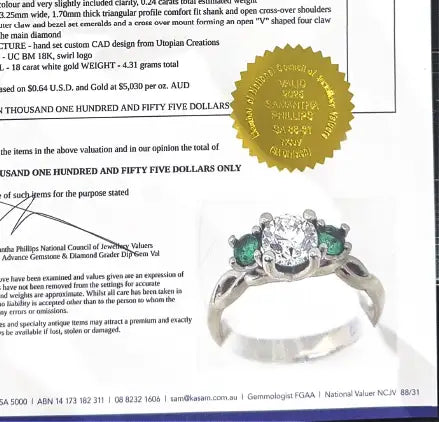

- 01A full written descriptionThe metal, the stones, their measurements and quality, and the workmanship — detailed enough to replace the piece like for like.

- 02Photographs of the pieceClear images form part of the record — they matter for identification and for a smooth claim.

- 03A retail replacement valueWhat it would cost to make or buy the piece again today — the figure insurance is based on. Not what you paid, and not what you would get selling it.

- 04A dated, signed certificateIssued by the valuer, ready to hand straight to your insurer.

Keep the certificate and photos somewhere safe, away from the jewellery itself — if a piece is ever lost or stolen, that paperwork is what makes the claim straightforward.

Worth knowing

Two things people miss.

Check your policy actually covers jewellery. Many home and contents policies have a low per-item limit — often lower than a single good ring — and cover away from home is not a given. High-value pieces usually need to be listed individually, and that is where the valuation comes in.

A receipt is not a valuation. Insurers generally want a formal valuation document, not a purchase receipt — a receipt records what you paid once, not what replacement costs now.

None of this is insurance advice — your policy and insurer set the rules. But a current, independent valuation is the piece of the puzzle we can help with, and the one most people put off.

The first step

Get it valued properly.

Bring your piece in and we will arrange an independent valuation — and tell you the cost and turnaround up front.